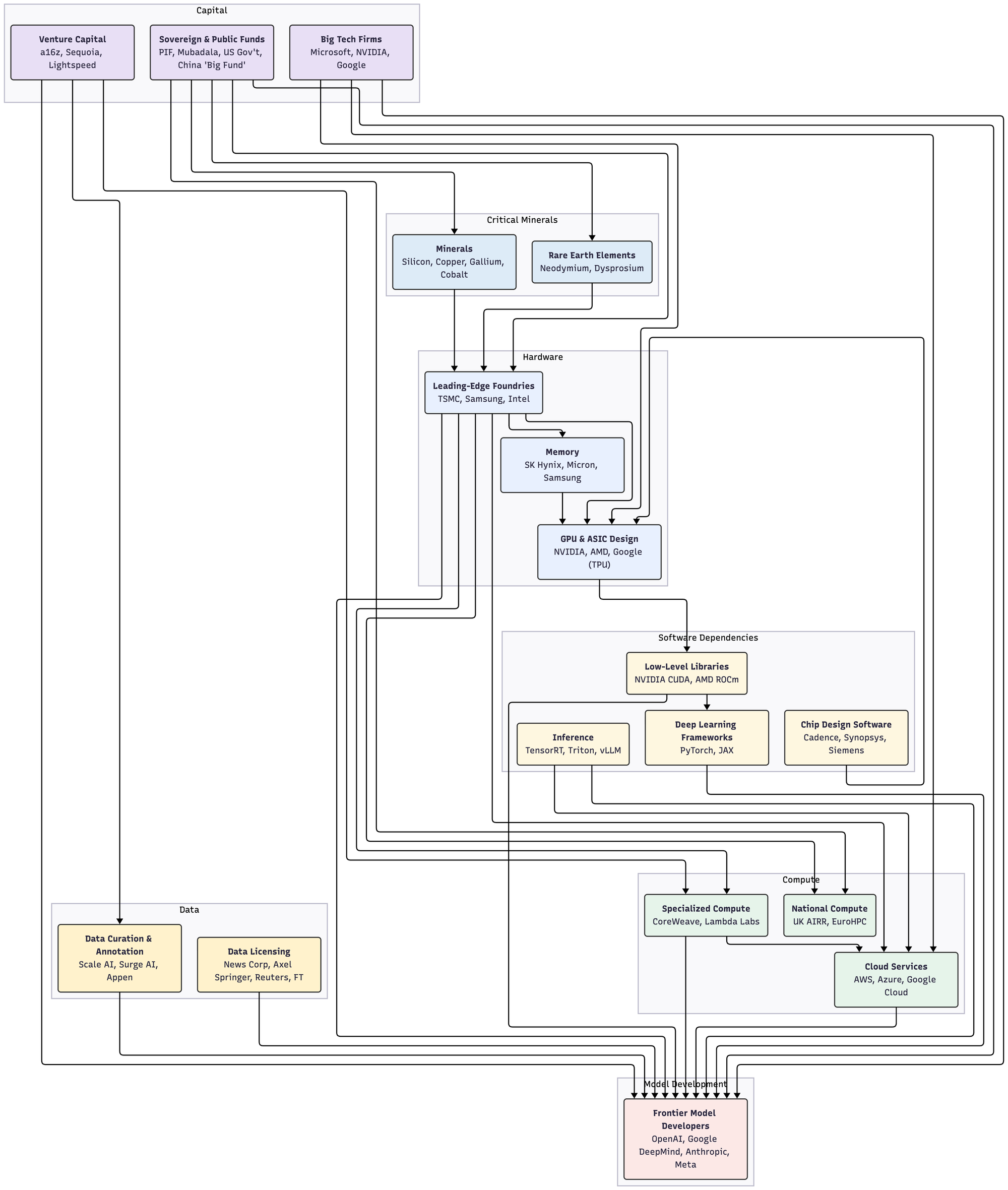

An Evolving AI Supply Chain

How is the structure of the frontier AI model supply chain changing? How are new developments across capital investments, critical minerals, datasets, compute services, and hardware influencing each other?

Download the new report, which explores these questions.

This paper identifies key areas of change and uncertainty across the frontier AI model development supply chain and investigates how disparate supply chain segments are interconnected.

Over the next decade, the AI supply chain is likely to become more multi-polar as nations and companies invest in creating alternative options for computing and hardware to support frontier-scale AI development. The growing use of AI to support model and hardware development will also lead the supply chain in new and unexpected directions. Geopolitical maneuvering will intensify due to the perceived economic and national security stakes of owning access to and jurisdiction over varous parts of the AI supply chain.

Data: Scarcity and Cost

• Increasing data scarcity, the rise of synthetic and multi-modal data, and complex licensing agreements are increasing the cost barrier to finding and using high-quality data

• Over-reliance on synthetic data could pose significant challenges. The market for specialized data curation and processing companies is growing rapidly

Compute: Optionality and Control

• Computational power is concentrated among a few major cloud providers, while there is explosive growth in demand for compute resources

• As a result, a market in specialized AI clouds ("neoclouds") is growing, countries are pursuing "cloud sovereignty," and decentralized compute is growing as an area of research

Hardware: Specialization and Geopolitics

• Advanced chips, high-bandwidth memory, and network interconnects are critical inputs into AI development

• NVIDIA maintains a dominant market position supported by its CUDA platform. Meanwhile, custom ASICs are attracting increasing investment and usage from frontier model developers

• The U.S. has attempted to restrict China’s access to cutting-edge hardware, but China has made significant progress in their domestic hardware ecosystem despite these restrictions

Critical Minerals: Concentration and Negotiation

• Various critical minerals are necessary for manufacturing hardware, building data centers, and supplying power to data centers. Production and processing of these minerals is highly concentrated, particularly in China

• Throughout 2025, the U.S. government has been attempting to reduce dependence on China through investments to support domestic minerals companies, as well as engagements with countries including Ukraine and Australia

Capital: Ownership and Interdependency

• Immense capital investment is flowing into the AI supply chain, driven by venture and growth firms, hyperscalers, and sovereign wealth funds

• Strategic partnerships and blended financing agreements are creating deeply intertwined alliances between hardware providers, model developers, and governments

Download the new report to read more. Subscribe to keep up with future updates on these topics and drop a note if you or your organization are interested in working together.

SUBSCRIBE

...to keep up with research updates and announcements